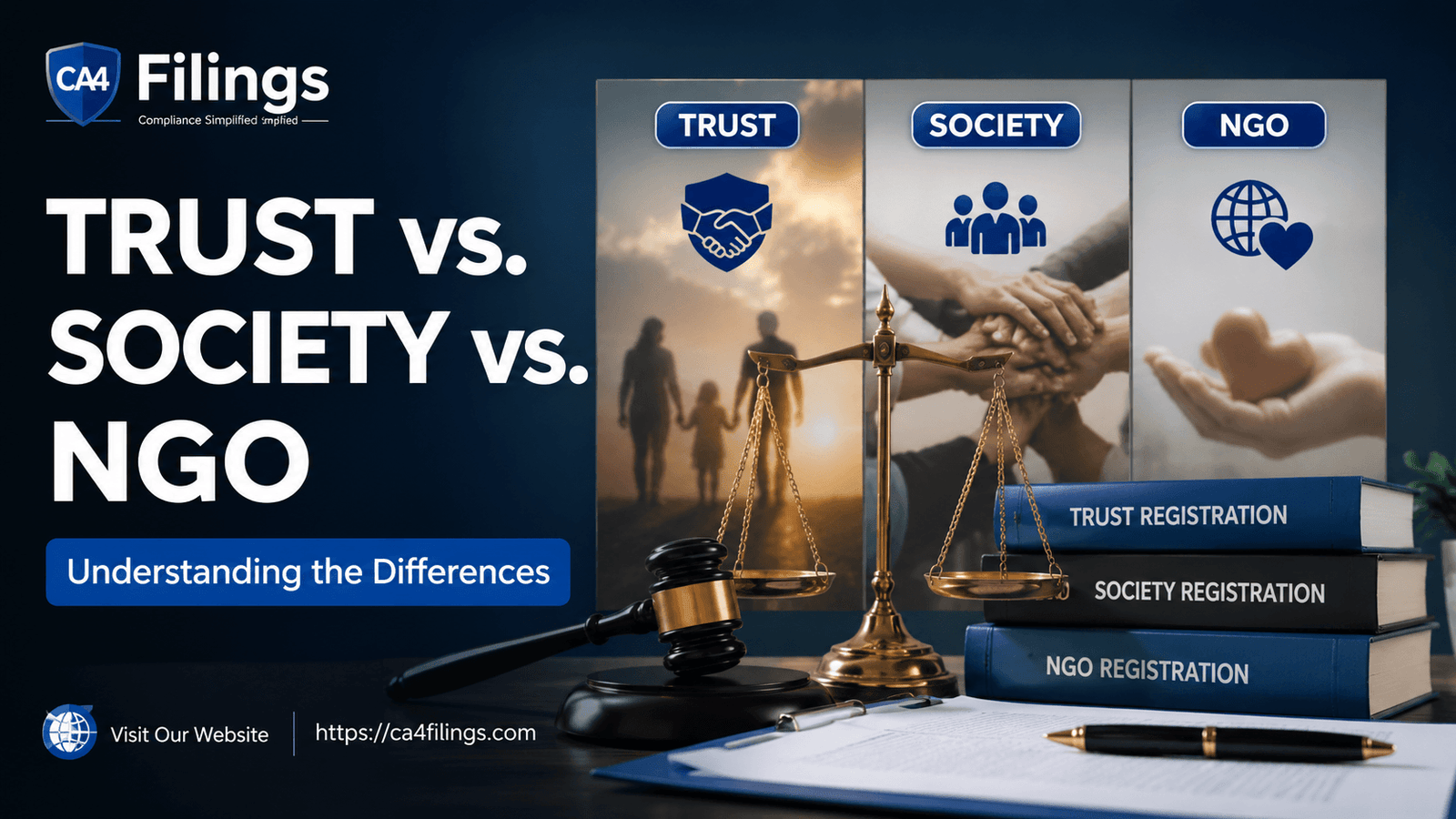

Trust vs. Society vs. NGO: Understanding the Differences

Discover the legal setup, governance, and compliance variations in Trust vs. Society vs. NGO: Understanding the Differences by CA4Filings experts.

When well-meaning individuals or corporate groups decide to give back to the community, they often find themselves trapped in a web of legal terminologies. In my extensive practice as a Chartered Accountant at CA4Filings, the most common puzzle entrepreneurs ask me to solve is: "Should I set up a trust, a society, or an NGO" If you are asking yourself the same question, let me assure you that you are not alone. Choosing the right structural format for your philanthropic venture is critical, as it dictates how you operate, manage your funds, and meet tax compliances. In this comprehensive guide, we will unpack the complexities of Trust vs. Society vs. NGO: Understanding the Differences so that you can pick the setup that best matches your long-term goals.

Before we jump into the technical operational differences, it is important to lay down a solid baseline. Many people treat "NGO" as a distinct third legal category, which is a common misconception. An NGO or Non-Governmental Organization is a broad, umbrella term that encompasses any non-profit entity dedicated to a social cause, community development, or social impact. In India, if you want to operate a non-profit NGO, you must legally register it under one of three primary frameworks: a Public Charitable Trust, a Registered Society, or a Section 8 Company. At CA4Filings, we specialize in seamless Trust Registration and handling all forms of non-profit incorporation, ensuring that your noble mission starts on a legally airtight footing without any administrative delays.

Demystifying the Non-Profit Frameworks

To fully grasp the dynamics of Trust vs. Society vs. NGO: Understanding the Differences, we must look at the distinct legal structures that give life to an NGO. Let us break down the definition, purpose, and governing laws of the two main traditional routes chosen by founders across Indian communities.

1. Public Charitable Trust

A Public Charitable Trust is one of the oldest and simplest forms of non-profit structures in India. It is usually formed when a property owner (the author or settlor) dedicates a certain property or sum of money for public charitable purposes. This arrangement is formalized through a legal document known as a Trust Deed. Trusts are primarily governed by the Indian Trusts Act, 1882 for private setups, while public religious or charitable trusts are regulated by state-specific legislations, such as the Bombay Public Trusts Act, 1950 or similar local state statutes.

2. Registered Society

A society is a more democratic setup formed when a group of individuals comes together for a common, mutual purpose. This could range from promoting science, arts, literature, or executing broad-based community development projects. Societies are registered under the Societies Registration Act, 1860 (or corresponding state amendments). Unlike a trust, which revolves around a property or a small group of founders, a society is built on a membership model and runs on a well-defined Memorandum of Association (MoA) and Rules and Regulations.

Expert CA Insight: Think of a Trust as a "one-man or family-centric" initiative where control remains tight, whereas a Society is akin to a "club or democratic assembly" where the power shifts with periodic elections.

Trust vs. Society vs. NGO: Understanding the Differences in Core Governance

When clients visit the CA4Filings office to choose between these entities, we focus heavily on governance, accountability, and operational flexibility. Let us evaluate how these options stack up across key structural elements.

Minimum Number of Members and Management

To form a public charitable trust, you require a minimum of two individuals: the settlor and a trustee. The settlor cannot generally be the sole trustee, but they can definitely name a board of trustees to manage the trust resources. The control remains deeply consolidated, and trustees often hold office for their lifetime or as specified in the deed, ensuring continuity of the initial mission.

On the flip side, a society demands a minimum of seven members to come together at the national level. These members form a Governing Body or Managing Committee. This committee is subject to regular elections. If you want a setup where external members can join, share responsibilities, and vote on future initiatives, a society provides that democratic infrastructure.

Control and Accountability

From an audit and transparency perspective, a society requires a higher degree of ongoing administrative maintenance. You are legally required to file a list of the governing body members annually with the Registrar of Societies, along with audited accounts in many states. This keeps governance dynamic but can sometimes lead to internal politics or disputes over control during elections.

A trust offers a more stable and closed governance structure. Since there are no general body members to vote out the founders, the original vision of the philanthropic work is rarely disrupted by internal administrative coups. This makes it an ideal option for families or corporate houses that want absolute control over their dedicated donation funds.

Tax Implications, Funding, and Social Impact

Whether you establish a trust or a society to operationalize your NGO, the tax laws treat both categories similarly under the Income Tax Act, 1961. To attract corporate donation funds or secure institutional support, your non-profit must actively secure tax exemptions. This involves applying for Section 12AB (for exemption on the organization's income) and Section 80G (which allows donors to claim deductions on their corporate or individual contributions).

Both structures are fully eligible to access these tax benefits and receive foreign funding under the Foreign Contribution Regulation Act (FCRA), provided they fulfill the required transparency criteria. Therefore, your choice between a trust and a society should not be based on tax benefits, but rather on how you intend to scale your goals and manage internal roles.

Step-by-Step Selection Guide by CA4Filings

If you are still on the fence trying to resolve the Trust vs. Society vs. NGO: Understanding the Differences dilemma, follow this simple advisory checklist from our compliance experts:

Analyze Your Control Preference: If you want to retain absolute, centralized authority over the institution without worrying about being outvoted, opt for a Trust.

Evaluate Your Team Size: If you have a large network of institutional volunteers, professionals, or community leaders who expect equal voting rights, choose a Society.

Define the Purpose: For running specific static institutions like schools, hospitals, or orphanages, a trust layout works seamlessly. For running dynamic, member-driven initiatives like athletic clubs, literary forums, or traders' associations, a society is ideal.

Consider Setup Timeline and Geography: Trust creation is generally faster and involves less paperwork compared to a society, which requires extensive verification of multiple members' identities across states.

Frequently Asked Questions (FAQs)

Q1: Can an NGO register as both a Trust and a Society simultaneously?

No. An NGO must choose one legal form for its incorporation. It can be registered either as a Public Charitable Trust, a Registered Society, or a Section 8 Company. It cannot combine these distinct legal identities.

Q2: Is a Trust or a Society better for receiving corporate CSR funds?

Both formats are equally eligible to receive Corporate Social Responsibility (CSR) funding. Corporates look for valid 12AB and 80G registrations, a clean track record of financial accountability, and active CSR-1 registration with the Ministry of Corporate Affairs, rather than the specific entity type.

Q3: Can family members be trustees in a Public Charitable Trust?

Yes, close family members can legally be part of the board of trustees. However, to ensure absolute transparency and build strong credibility with public donors, it is highly recommended to include independent, non-related professionals on your board.

Q4: Can a society be dissolved easily if members lose interest?

Dissolving a society requires a specific vote passed by at least three-fourths of its members. Upon dissolution, any remaining funds or properties cannot be distributed among the members; they must be transferred to another society with similar charitable goals.

Launching Your Mission Safely

Navigating the complex landscape of Trust vs. Society vs. NGO: Understanding the Differences does not have to be overwhelming. At the end of the day, an NGO is simply the vehicle for your charitable heart, while the choice between a trust and a society determines how that vehicle is steered. If you want a quick, secure setup with lifelong control, a trust is your best match. If you seek a democratic, member-driven infrastructure built for wide community participation, a society fits perfectly.

Let CA4Filings Handle Your Non-Profit Incorporation!

Do not let legal paperwork delay your desire to create a lasting social impact. At CA4Filings, our seasoned legal and financial experts handle everything from drafting custom Trust Deeds and drafting Society Memorandums to securing PAN, TAN, 12AB, and 80G tax exemptions. Let us take care of the compliance and corporate bureaucracy while you focus entirely on your community missions.

Latest Updates

ca4filings.com Services

-registration.png)