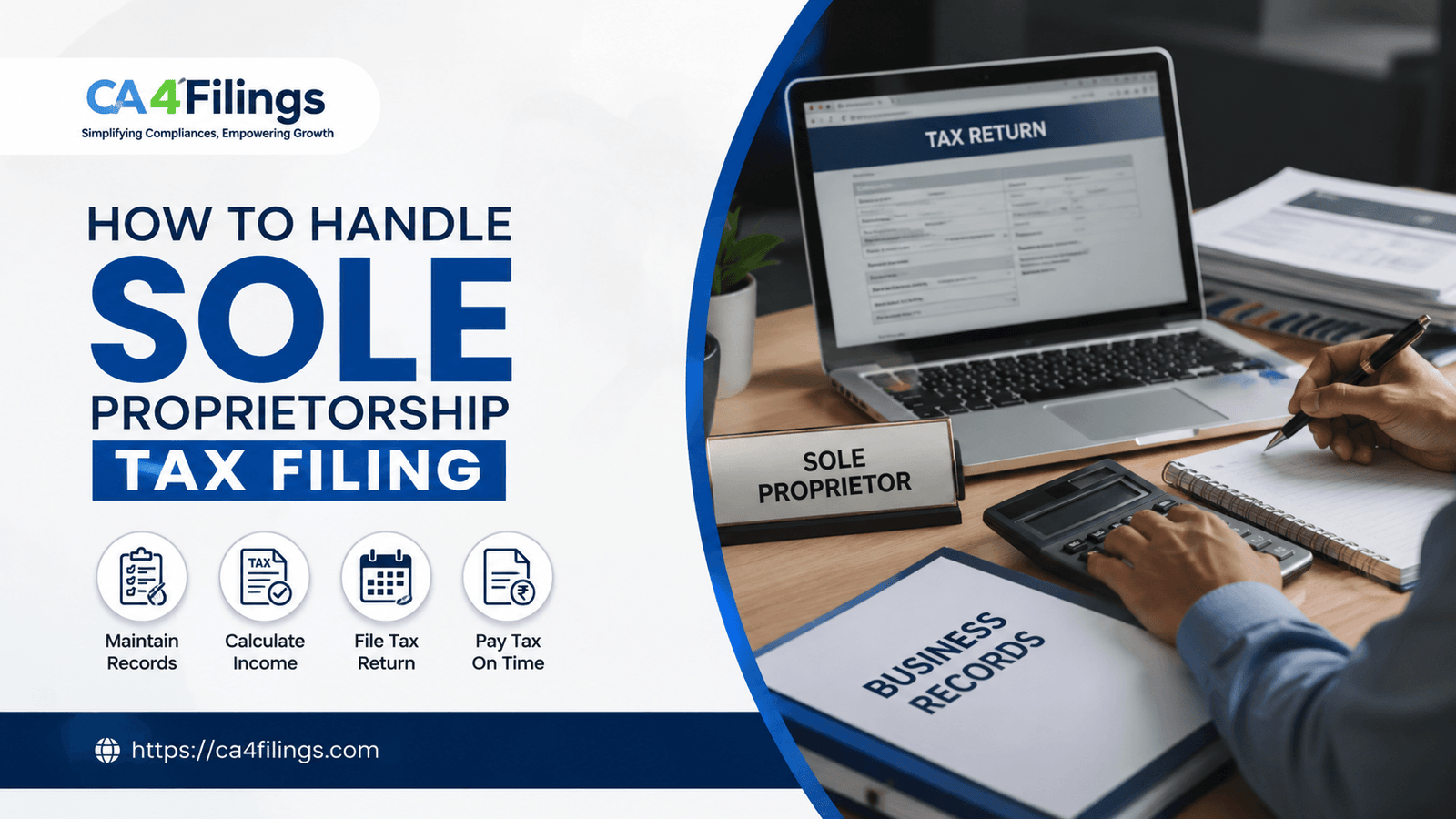

How to Handle Sole Proprietorship Tax Filing

Struggling with taxes? Learn How to Handle Sole Proprietorship Tax Filing in India with this expert guide from CA4Filings. Master your tax obligations.

Running a business as a sole proprietor is an exciting journey, but it comes with the responsibility of managing your own finances and compliance. If you are just starting out, ensuring you have completed your Sole Proprietorship Registration is the first step toward building a legitimate foundation for your enterprise. Once your business is set up, the next big hurdle is understanding How to Handle Sole Proprietorship Tax Filing effectively. Many small business owners feel overwhelmed by the complexities of Indian tax laws, but with the right approach, it becomes a manageable part of your annual routine.

At CA4Filings, we guide thousands of entrepreneurs through the nuances of business taxation. Understanding How to Handle Sole Proprietorship Tax Filing doesn't just keep you compliant; it also helps you optimize your financial health and maximize your savings.

Why Sole Proprietorship Tax Filing is Different

In India, a sole proprietorship is not a separate legal entity from the owner. This means your business income is legally identical to your personal income. Unlike a private limited company, where you might draw a formal salary, as a sole proprietor, you are the business. Consequently, your self-employment income is taxed according to the income tax slab rates applicable to individuals.

Because there is no legal separation between you and your business, you must be meticulous in tracking your financial records throughout the year. How to Handle Sole Proprietorship Tax Filing successfully starts with maintaining clear, organized books of accounts from day one, rather than scrambling at the last minute when the filing deadline looms.

Essential Steps for Proper Tax Compliance

1. Maintain Comprehensive Financial Records

Before you begin the filing process, gather all your data. You need a transparent record of every business receipt and payment. Even if you aren't legally required to maintain formal audits until your turnover exceeds a specific threshold, having organized bank statements and invoices is crucial for substantiating your claims and identifying potential tax deductions.

2. Identifying Legitimate Deductible Expenses

One of the most effective ways to reduce your tax liability is by identifying all legitimate business expenses. As a small business owner, you can deduct costs directly related to running your trade, which reduces your taxable net profit. These typically include:

Office Expenses: Rent, electricity, and internet bills related to your workspace.

Operational Costs: Salaries paid to employees and payments to contractors.

Marketing: Costs incurred for advertising, website maintenance, or branding.

Professional Fees: Payments made for accounting, legal, or consulting services.

Depreciation: The wear and tear on business assets like machinery, laptops, or office furniture.

Keeping track of these business expenses allows you to calculate your net taxable profit more accurately, ultimately leading to better tax savings.

3. Understanding Presumptive Taxation

Many sole proprietors in India can opt for the Presumptive Taxation Scheme under Section 44AD or 44ADA of the Income Tax Act. This is a game-changer for many small businesses. Instead of maintaining exhaustive books of accounts, you can declare a fixed percentage of your turnover as profit. Learning How to Handle Sole Proprietorship Tax Filing using this method can save you significant time and professional fees, provided you meet the specific eligibility criteria.

Expert Tax Tips for Sole Proprietors

Tax planning is not a one-time event; it is a year-long strategy. To handle your taxes better and ensure you are not paying more than your fair share, consider these expert tips:

Separate Business and Personal Finances: Never mix your personal and business bank accounts. It creates a nightmare during reconciliation and makes it significantly harder to prove business expenses if you are ever scrutinized by tax authorities.

Utilize All Tax Deductions: Don't forget personal tax deductions under Chapter VI-A (such as Section 80C for investments or 80D for health insurance), which apply to you as an individual taxpayer.

Stay Ahead of Deadlines: Missing the Income Tax Return (ITR) deadline attracts penalties and interest. Always aim to file well ahead of the due date to avoid the last-minute rush.

Frequently Asked Questions

Do I need a separate PAN for my sole proprietorship?

No, a sole proprietorship uses the individual proprietor's personal PAN. The business and the owner are legally considered the same entity.

Which ITR form should I use?

Generally, proprietorships use ITR-3 if they have income from a business or profession, or ITR-4 if they opt for the Presumptive Taxation Scheme.

Are all business expenses tax-deductible?

Only those expenses incurred "wholly and exclusively" for the purpose of your business are deductible. Personal expenses—such as groceries or home rent not used for business—cannot be claimed.

How can CA4Filings help me?

We provide end-to-end support, from initial registration to tax planning and final ITR filing, ensuring you remain compliant and tax-efficient throughout the financial year.

Understanding How to Handle Sole Proprietorship Tax Filing is a critical skill for every entrepreneur. By maintaining clean records, understanding your deductions, and choosing the right tax scheme, you can focus on growing your business while keeping the taxman happy. Remember, you don't have to navigate these complex regulations alone. At CA4Filings, we are dedicated to simplifying the tax journey for every small business owner. Contact us today to ensure your tax filing is seamless, accurate, and stress-free.

Latest Updates

ca4filings.com Services

-registration.png)