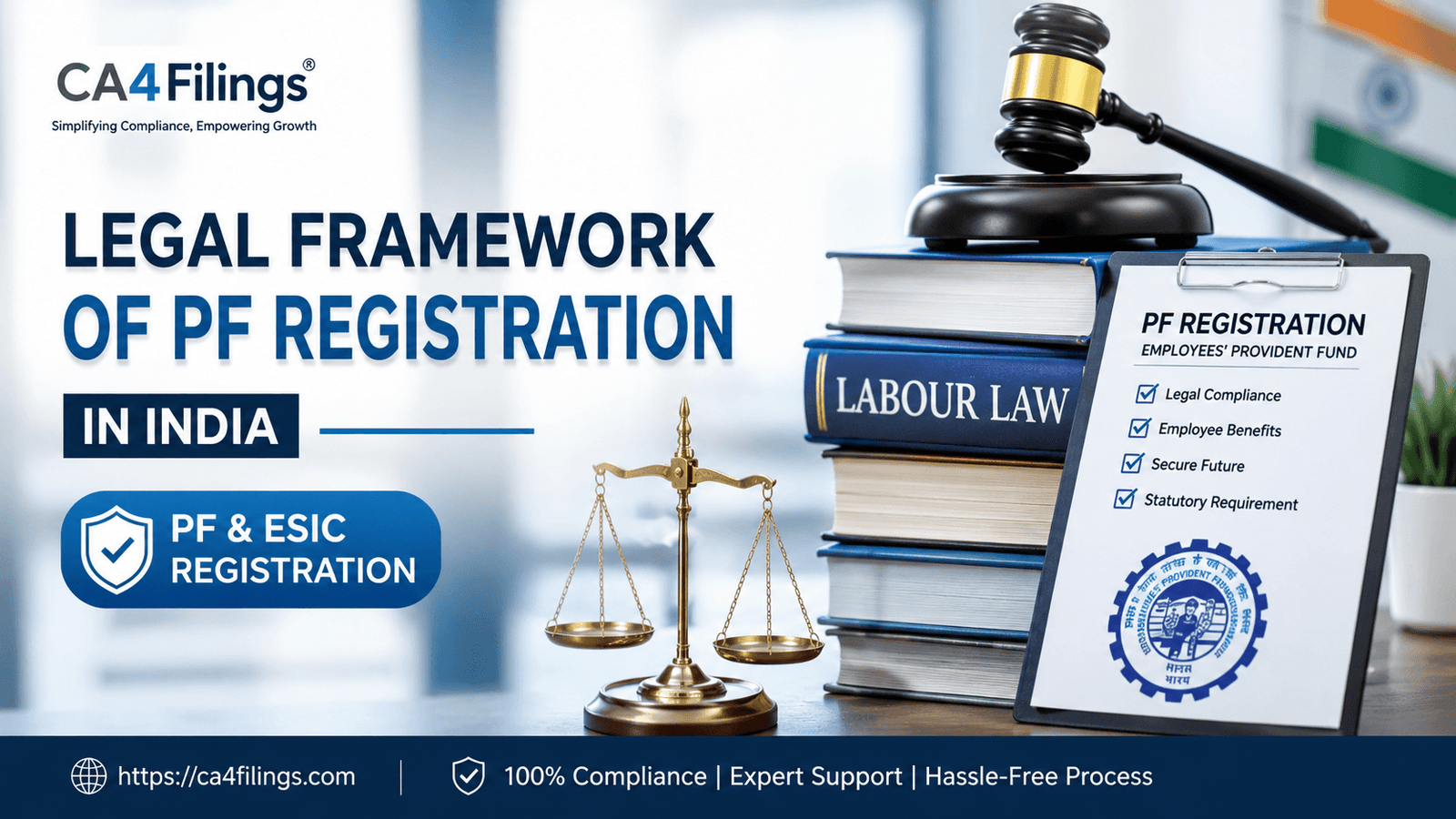

Exploring the Legal Framework of PF Registration in India

Understanding the compliance landscape is vital for growth. Start Exploring the Legal Framework of PF Registration in India with CA4Filings today.

Running a business in India is an exciting journey, but it comes with a fair share of compliance responsibilities. One of the most important aspects for any growing organization is ensuring your employees are protected and your statutory obligations are met. If you are a business owner, Exploring the Legal Framework of PF Registration in India is not just a suggestion; it is a regulatory mandate that ensures your venture remains on the right side of the law. Managing these complexities can be daunting, which is why we at CA4Filings simplify the process through our professional PF & ESIC Registration services, ensuring you focus on your core business while we handle the paperwork.

Understanding the Statutory Basis of Provident Fund

The Provident Fund (PF) is governed primarily by the Employees' Provident Funds and Miscellaneous Provisions Act, 1952. As a Chartered Accountant, I often tell my clients that this act was designed with a simple yet noble vision: to provide financial security to employees during their retirement or in times of unforeseen circumstances.

When you are Exploring the Legal Framework of PF Registration in India, you will find that the law applies to every establishment which employs 20 or more persons. However, don't let that number mislead you. Even if you have fewer than 20 employees, you can opt for voluntary registration to provide better benefits, which often helps in attracting top-tier talent.

Why Compliance is Non-Negotiable

From a professional standpoint, compliance is about risk mitigation. The EPFO (Employees' Provident Fund Organization) has become increasingly digital, and their surveillance systems are robust. Non-compliance can lead to:

Heavy penalties and interest on delayed payments.

Legal repercussions that can disrupt business operations.

Damage to the company’s reputation among employees.

Difficulty in participating in government tenders or contracts.

When you start Exploring the Legal Framework of PF Registration in India, you realize that timely filing is not just about avoiding fines; it is about building trust with your workforce.

Exploring the Legal Framework of PF Registration in India: The Eligibility Criteria

Before jumping into the registration portal, let’s look at the foundational rules. The Act applies to:

Establishments employing 20+ persons: This is the standard threshold.

Voluntary Registration: Smaller firms can register if both the employer and the majority of employees consent to it.

Nature of Employment: The provisions cover all employees drawing a basic salary and dearness allowance up to a specific limit (currently ₹15,000 per month for mandatory coverage, though many companies cover higher salaries).

The Step-by-Step Registration Process

Many business owners get stuck at the technicalities of the Unified Portal. While Exploring the Legal Framework of PF Registration in India, it is crucial to understand that the process is entirely online.

Step 1: Obtain a Digital Signature Certificate (DSC): The employer’s authorized signatory must have a valid Class 3 DSC.

Step 2: Employer Registration: Visit the EPFO Unified Portal and fill in the establishment details.

Step 3: Verification: The system will verify the data through PAN and Aadhaar linkages.

Step 4: Submission: Once the details are verified, a temporary password is sent to the registered mobile number. After changing the password, the registration application is submitted.

Step 5: Approval: Once the department approves the application, the establishment receives the Establishment Code, which is your unique identity for all PF-related filings.

Common Pitfalls to Avoid

In my experience at CA4Filings, I have seen businesses struggle with basic errors. Here is where most go wrong:

Incorrect KYC: Mismatched names or dates of birth between Aadhaar and bank records are the primary reasons for claim rejections.

Delayed Contributions: The statutory deadline is the 15th of the following month. Always aim to pay by the 10th to avoid any technical delays.

Ignoring Wage Ceiling Rules: Understanding what constitutes "basic pay" is vital to ensure you are contributing the correct percentage ($12\%$).

FAQs: Clarifying Your Doubts

1. Is it mandatory to register if I have fewer than 20 employees?

No, it is not mandatory under the Act, but you can register voluntarily to provide better social security to your staff.

2. Can an employer stop PF deductions?

Once an establishment is registered, it cannot unilaterally stop contributions unless the establishment is closed or the number of employees falls significantly below the threshold for an extended period, subject to EPFO approval.

3. What happens if I fail to register on time?

You may be liable to pay damages and interest on the unpaid contributions. In severe cases, the authorities can initiate recovery proceedings.

4. How does Exploring the Legal Framework of PF Registration in India help in long-term growth?

It keeps your business audit-ready, prevents surprise penalties, and ensures you are a law-abiding employer, which is essential for scaling up.

Navigating the statutory maze is an essential part of entrepreneurship. While Exploring the Legal Framework of PF Registration in India might seem like a complex chore, it is a foundation for a stable and ethical organization. You don't have to do it alone. At CA4Filings, we specialize in making these transitions smooth and stress-free for business owners.

Latest Updates

ca4filings.com Services

-registration.png)