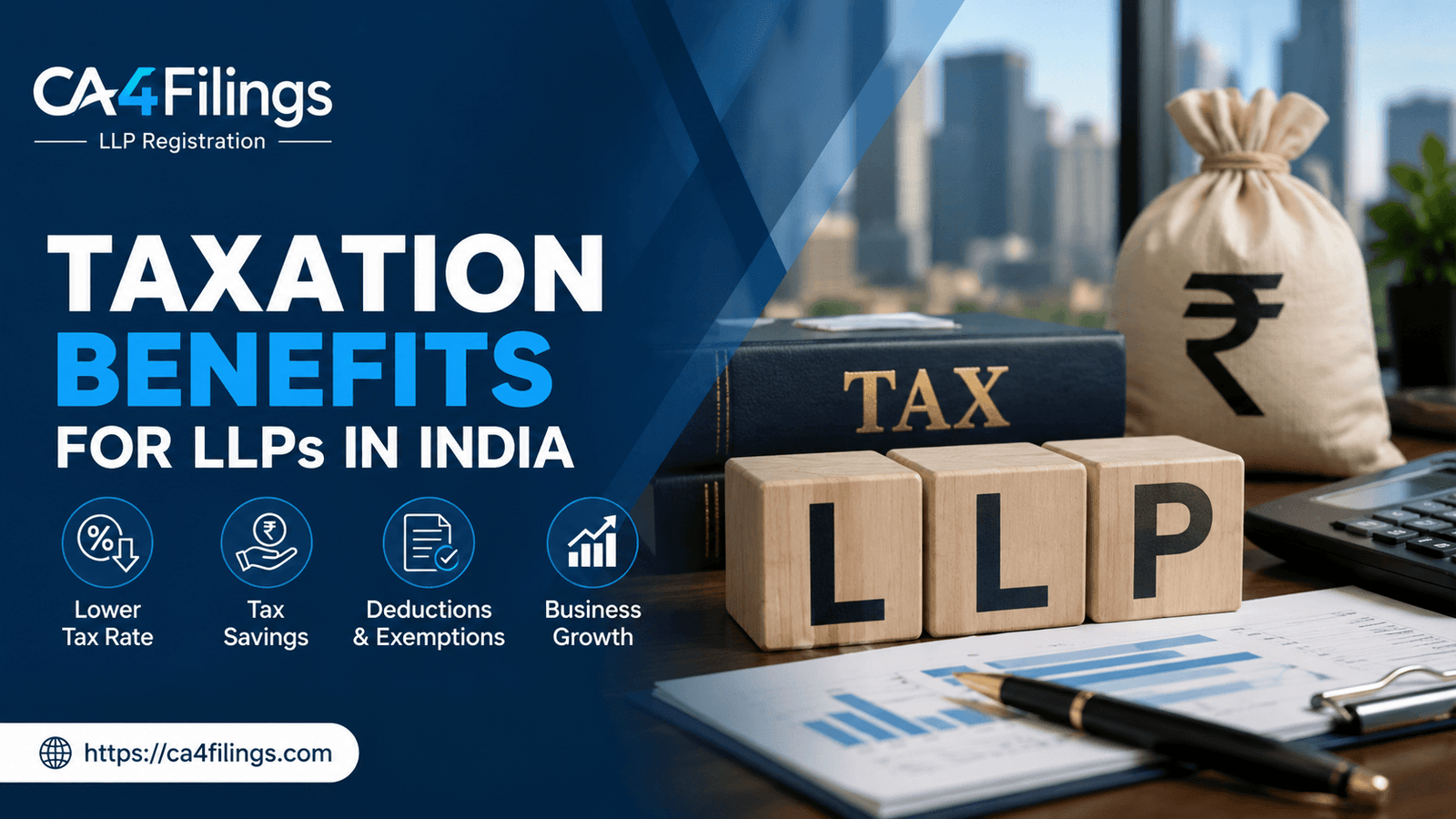

Taxation Benefits for LLPs in India

Discover the ultimate taxation benefits for LLPs in India. Learn about tax rates, pass-through taxation, and expert tax savings strategies from CA4Filings.

When starting a new business venture in India, choosing the right business structure is one of the most critical decisions an entrepreneur has to make. While traditional partnership firms offer simplicity and Private Limited Companies bring robust credibility, the Limited Liability Partnership (LLP) framework brilliantly bridges the gap. It provides the structured operational ease of a corporate entity while keeping regulatory compliance burdens light. At CA4Filings, we constantly meet founders who look to optimize their tax strategies right from day one. Understanding the specific Taxation Benefits for LLPs in India can become your ultimate tool to maximize your bottom line and effectively retain hard-earned profits within your business ecosystem.

Many business owners mistakenly believe that corporate tax savings are exclusively reserved for large, equity-backed private limited companies. This is far from the truth. In fact, when you look closely at how the Income Tax Act treats different entities, Limited Liability Partnerships enjoy distinct operational advantages that can help optimize and streamline tax obligations effortlessly. If you are still in the planning phase, executing your LLP Registration early on ensures that you lay down a compliant, tax-efficient foundation for all your future commercial transactions. Let us dive deep into the specific mechanisms that make taxation benefits for LLPs a highly lucrative option for modern businesses in India.

Understanding the Tax Structure and Tax Rates for LLPs

To fully grasp the Taxation Benefits for LLPs in India, we must first look at the basic tax rate structure. Unlike individuals or HUFs, an LLP is taxed as a distinct legal entity at a flat rate. There is no slab-wise basic exemption limit applicable here.

Flat Tax Rates Breakdown

For the assessment year, LLPs are taxed at a base rate of 30% on their total net income. While this might appear identical to the standard corporate rate at first glance, the secondary components offer significant relief:

Surcharge: A flat surcharge of 12% is applicable only if the total income of the LLP exceeds ₹1 Crore. For companies, surcharges kick in at lower comparative scales or vary steeply depending on the chosen tax regime.

Health and Education Cess: A standard 4% cess is levied on the aggregate of the income tax and surcharge.

This transparent, predictable environment regarding tax rates allows founders to forecast cash flows easily without navigating the multi-tiered complexities often found in corporate balance sheets.

The Power of Deductions: Interest and Salary to Partners

One of the most profound Taxation Benefits for LLPs in India lies in how profit distribution is handled. In a traditional company, taking money out requires routeing it through structured payroll or declaring dividends, which are subject to stringent corporate compliance. In an LLP, the partners can directly claim deductions for payments made to themselves as interest on capital or working salary.

1. Remuneration to Working Partners

LLPs can pay salaries, bonuses, and commissions to their working partners and claim it as a business expense, thereby reducing the net taxable income of the firm. However, this is governed strictly by Section 40(b) of the Income Tax Act. The maximum permissible deduction for partner remuneration is calculated via a structured book-profit formula:

On the first ₹3,00,000 of book profit: ₹1,50,000 or 90% of book profit (whichever is more)

On the balance of book profit: 60% of the remaining book profit

2. Interest on Capital Contributed

If partners have infused capital into the firm, the LLP can pay them interest up to a maximum limit of 12% per annum. This payment is completely deductible from the LLP’s gross earnings, serving as an excellent mechanism for legitimate tax savings.

Exemption of Profit Distribution: No Double Taxation

When an Indian private company distributes its profits to its shareholders, the process triggers complex taxation scenarios. However, for LLPs in India, the profit distribution model is incredibly elegant due to the concept of single-layer taxation.

Once the LLP pays its flat 30% tax (plus applicable cess and surcharge) on its net taxable income, the remaining profits are distributed directly among the partners based on their agreed profit-sharing ratio. Under Section 10(2A) of the Income Tax Act, this distributed share of profit is completely exempt from tax in the individual hands of the partners. This ensures that your hard-earned corporate revenue is never subjected to unfair double taxation, a massive benefit when compared to corporate dividend distribution models.

Expert Insight from CA4Filings: While an LLP is treated as a separate legal entity for tax assessment purposes rather than enjoying pure pass-through taxation (like partnerships do in some Western nations), the tax-free nature of profit distribution under Section 10(2A) effectively mirrors the best parts of pass-through benefits by keeping the individual partners immune from extra tax liabilities on their profit shares.

Flexibility in Carry Forward Losses and Asset Management

Every business goes through operational ups and downs, especially during its initial startup years. The ability to manage business losses effectively is a cornerstone of smart corporate tax planning. LLPs score exceptionally high on this front, offering long-term stability and resilience.

Unabsorbed Depreciation and Business Losses

An LLP is fully permitted to carry forward losses and unabsorbed depreciation to offset against future profitable years.

Business Losses: Can be carried forward for up to 8 consecutive assessment years and can be set off against future business profits.

Unabsorbed Depreciation: Can be carried forward indefinitely until it is completely absorbed by future profits.

This ensures that your early-stage investments and initial operational struggles actively lower your tax liabilities once your business gains commercial traction.

Comparing LLP Taxation vs. Private Limited Company Taxation

To help you visualize the real-world impact, let's break down how taxation benefits differ between an LLP and a Private Limited Company:

| Tax Parameter | Limited Liability Partnership (LLP) | Private Limited Company |

|---|---|---|

| Basic Tax Rate | Flat 30% | 22% or 15% (under special new regimes) |

| Profit Extraction Tax | Exempt under Section 10(2A) for partners | Taxable in the hands of shareholders as Dividends |

| Surcharge Threshold | Applies only if income exceeds ₹1 Crore | Applies starting from ₹1 Crore up to ₹10 Crores |

| Compliance Audit | Mandatory only if turnover > ₹40 L or capital > ₹25 L | Mandatory from year one regardless of turnover |

Frequently Asked Questions (FAQs)

1. Is Minimum Alternate Tax (MAT) applicable to LLPs in India?

Instead of MAT, LLPs are subject to Alternative Minimum Tax (AMT) under Section 115JC. If the regular income tax payable is less than 18.5% (plus cess/surcharge) of the adjusted total income, the LLP pays AMT at 18.5%. This AMT paid can be carried forward as a credit to offset regular tax liabilities for up to 15 subsequent years.

2. Can an LLP claim deductions for loans taken from partners?

Yes. If a partner provides a formal loan to the LLP beyond their initial capital contribution, the LLP can pay interest on that loan. As long as it aligns with commercial terms and complies with the LLP agreement, it can be claimed as a deductible business expense.

3. Can a salaried individual become a partner in an LLP and get tax benefits?

Yes, a salaried individual can become a partner. However, they can only receive their tax-free share of profits. To receive a deductible salary or remuneration from the LLP, they must be designated as a "working partner," which might conflict with their primary employment contract terms.

4. What happens to the carry forward losses if a partner leaves the LLP?

Unlike private companies where a significant change in shareholding can sometimes jeopardize tax losses, an LLP's carry forward losses remain intact within the entity, provided the overall structural identity of the LLP continues to exist under the law.

Streamline Your Business with CA4Filings

Leveraging the extensive Taxation Benefits for LLPs in India requires a deliberate approach, clean bookkeeping, and a deep understanding of current tax frameworks. By smartly structuring partner salaries, maximizing interest deductions, and utilizing long-term loss carry-forwards, you can easily establish an incredibly lean, tax-optimized business engine.

Latest Updates

ca4filings.com Services

-registration.png)