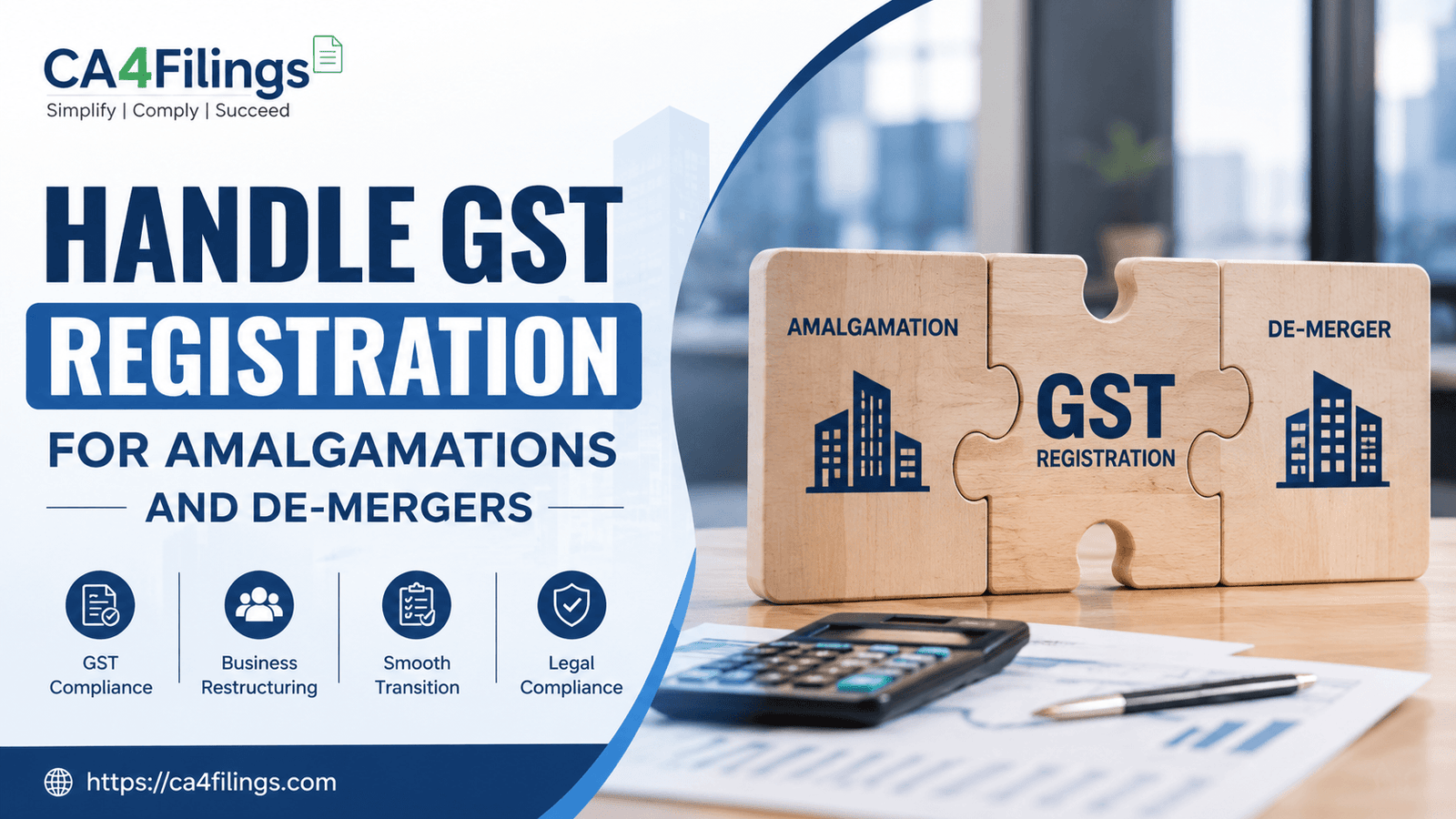

How to Handle GST Registration for Amalgamations and De-mergers

Navigating business restructuring? Learn exactly How to Handle GST Registration for Amalgamations and De-mergers to ensure compliance and avoid tax loss.

Restructuring your business through mergers, amalgamations, or demergers is a significant milestone, but it brings a unique set of compliance hurdles that often confuse even seasoned entrepreneurs. If you are navigating this transition, understanding How to Handle GST Registration for Amalgamations and De-mergers is critical to ensuring your operations remain uninterrupted. Whether you are scaling up or streamlining, getting your documentation and tax identity right from the start is non-negotiable. If you need expert help with your GST Registration, our team at CA4Filings is here to simplify the complex regulatory landscape for you.

Understanding the Legal Basis for Business Restructuring under GST

When a business undergoes a change in constitution—such as a merger or demerger—the GST law treats the entity's "identity" as having shifted. Under Section 22(3) of the CGST Act, 2017, when a business is transferred as a "going concern," the transferee (the entity taking over) becomes liable to be registered from the date of the transfer.

It is a common misconception that you can simply continue using the old GSTIN. In reality, because the GSTIN is linked to the PAN and the state of operations, a change in business ownership or structure typically necessitates fresh registration or, at the very least, significant amendments to your existing records.

How to Handle GST Registration for Amalgamations and De-mergers: The Step-by-Step Approach

Managing the transition requires a clear roadmap. Here is how we typically advise our clients at CA4Filings to handle these shifts:

1. Assessing the Need for New Registration

In cases of amalgamation or demerger, the "resulting company" often requires a new GST registration. Since the old entity may cease to exist (in a merger) or spin off a division (in a demerger), the new entity must apply for a fresh registration using its own PAN and incorporation documents.

2. Filing FORM GST ITC-02

This is the most crucial step for transferring your accumulated tax credits. If you don't file this correctly, your hard-earned Input Tax Credit (ITC) could be lost in the transition.

The Process: The transferor files Form GST ITC-02 on the common portal.

The Documentation: You must attach a certificate from a practicing Chartered Accountant or Cost Accountant. This certificate confirms that the restructuring scheme includes the transfer of all relevant liabilities.

The Acceptance: The transferee must log in to the portal and accept these details. Once accepted, the unutilized ITC is credited directly to the transferee’s electronic credit ledger.

3. Apportionment in Demergers

If you are specifically looking at How to Handle GST Registration for Amalgamations and De-mergers in the context of a demerger, remember that ITC cannot be transferred in total. It must be apportioned based on the ratio of the value of assets transferred, as defined in your NCLT-approved scheme.

Key Challenges Businesses Face

Invoicing Issues: If you continue issuing invoices under the old GSTIN after the effective date of the merger, your customers may face issues claiming ITC.

Unmatched ITC: Discrepancies between the transferor’s and transferee’s records can lead to audit flags.

Jurisdictional Changes: If your new entity operates in a state where the transferor was not registered, you must apply for a new registration in that state specifically.

Frequently Asked Questions (FAQs)

Can I transfer the cash balance in my Electronic Cash Ledger during a merger?

No. Unfortunately, the GST portal does not allow the transfer of the Electronic Cash Ledger balance via ITC-02. This balance can only be claimed as a refund by the transferor entity.

Is the transfer of business as a going concern taxable under GST?

Generally, the transfer of a business as a "going concern" is treated as an exempt service, provided the conditions under the relevant notifications are met. However, you must document this transition meticulously to avoid future litigation.

What happens if I forget to file ITC-02?

If you fail to file this form, the ITC remains stuck in the transferor’s account. Once the transferor’s registration is cancelled, retrieving that credit becomes a long, cumbersome legal process.

Do I need a new GSTIN if I am only changing the name of the company?

If the PAN remains the same, you can simply file an amendment (Form REG-14) for a name change. However, if the restructuring involves a change in PAN (as in most mergers), a fresh registration is mandatory.

Knowing How to Handle GST Registration for Amalgamations and De-mergers is about more than just paperwork; it is about protecting your company’s financial health and ensuring business continuity. From filing Form ITC-02 to securing the right certifications, every step matters.

At CA4Filings, we specialize in helping businesses navigate complex corporate restructuring and compliance. Don't let tax complexities hold back your growth. Reach out to our experts today, and let us handle your filings while you focus on taking your business to the next level.

Latest Updates

ca4filings.com Services

-registration.png)