Step-by-Step Guide to Applying for 12A Registration

Master the complete Step-by-Step Guide to Applying for 12A Registration in India. Learn the updated documentation, eligibility, and filing tips from CA4Filings.

Running a non-governmental organization (NGO) or a charitable trust in India is an incredibly noble journey, but it comes with its fair share of legal responsibilities. When we set up an organization to give back to society, we usually focus on the ground impact. However, to sustain that impact financially, you cannot afford to ignore the taxation aspect. This is where a critical legal framework comes into play: securing an Income Tax Exemption.

For any newly formed or existing charitable entity, learning a Step-by-Step Guide to Applying for 12A Registration is the absolute first milestone toward long-term survival. Without this, your hard-earned donations and grants will be heavily taxed at the maximum marginal rate (up to 30%+), heavily restricting your capability to do good work. Getting registered ensures that your institution's surplus income remains entirely exempt from tax, provided it is used strictly for charitable purposes. If you want to maximize your organization's credibility, you must bundle this step with 80G approval, which provides vital tax benefits to your donors. At CA4Filings, we help streamline this exact 12A and 80G Registration roadmap so that social leaders can focus purely on making a real difference without getting bogged down by legal complexities.

Understanding the Basics of 12A Registration

Before diving deep into the actual Registration Process, let’s break down exactly what this certification entails. Historically, under the Income Tax Act, 1961, Section 12A was a one-time, perpetual certificate granted to non-profit entities. However, the regulatory landscape has evolved to ensure higher transparency and curb tax evasion.

Under the updated guidelines, the old absolute lifetime validity is gone. Every charitable trust, society, or Section 8 company must now navigate a system that issues a time-bound registration. The law divides this into two broad categories:

Provisional Registration: Granted to newly established entities that have not yet commenced their operational, charitable activities. This serves as an initial permit valid for 3 tax years.

Regular/Final Registration: Granted to active organizations that have already started their operations. This is generally valid for 5 tax years and must be renewed periodically.

Securing this status establishes your organization as a legitimate entity in the eyes of the Income Tax Department, allowing you to legally claim exemptions on all voluntary contributions, interest payouts, and rental income.

Eligibility Criteria for Nonprofits

Not every organization that calls itself a "nonprofit" can simply fill out the Application Forms and receive a certificate. The tax department enforces strict baseline criteria to filter out commercial ventures disguised as charities.

To successfully clear the screening, your entity must align with the following requirements:

Genuine Charitable Purpose

Your organization's primary objectives must fall squarely within the definition of a "charitable purpose" under Indian law. This encompasses activities such as relief for the poor, advancement of education, medical relief, environmental preservation, or the advancement of any other object of general public utility.

No Profit Motive

The core intent of the entity must be entirely non-commercial. If your organization generates receipts from a trade, commerce, or business activity, it will only maintain its eligible status if those business receipts do not exceed 20% of the total receipts of the organization for that specific financial year. Furthermore, such business must be entirely incidental to achieving your primary charitable goals.

The Irrevocability Factor

This is an absolute dealbreaker. Your foundational rules must explicitly state that the trust or society is irrevocable. If the trust is dissolved, the remaining assets cannot go back to the founders or trustees; they must be transferred to another registered nonprofit entity holding a similar tax-exempt status.

Public Benefit vs. Private Gain

Private or family trusts established for the benefit of specific individuals, a single family, or a restrictive religious caste/community are completely excluded from receiving these tax benefits. Your activities must serve the general public interest openly.

Documentation Requirements for a Flawless Application

If there is one area where applications face instant rejection or heavy delay, it is paperwork. The department scrutinizes Legal Documents with a fine-tooth comb. To ensure your file moves smoothly, you need to compile a comprehensive dossier.

Here are the mandatory Documentation Requirements you must prepare before logging into the portal:

Foundational Instrument: A self-certified copy of the Trust Deed (for a public charitable trust), the Memorandum of Association and Rules (for a registered society), or the Incorporation Certificate (for a Section 8 Company).

Proof of Creation: Evidence proving the actual establishment of the organization.

PAN Card: A clear copy of the Permanent Account Number card issued specifically in the name of the Trust, Society, or Section 8 Company.

KYC of the Management: PAN cards, Aadhaar cards, mobile numbers, and email addresses of all the founders, trustees, or governing body members.

Registered Office Proof: A recent utility bill (electricity or water bill), a valid rent/lease agreement if the premises are rented, and a No Objection Certificate (NOC) from the actual property owner.

Activity Reports & Financials: For existing operational entities, detailed activity reports outlining the work done over the past three years, alongside audited financial statements (Balance Sheet and Profit & Loss accounts).

Other Statutory Registrations: Self-certified copies of your NGO Darpan ID registration or FCRA license, if applicable.

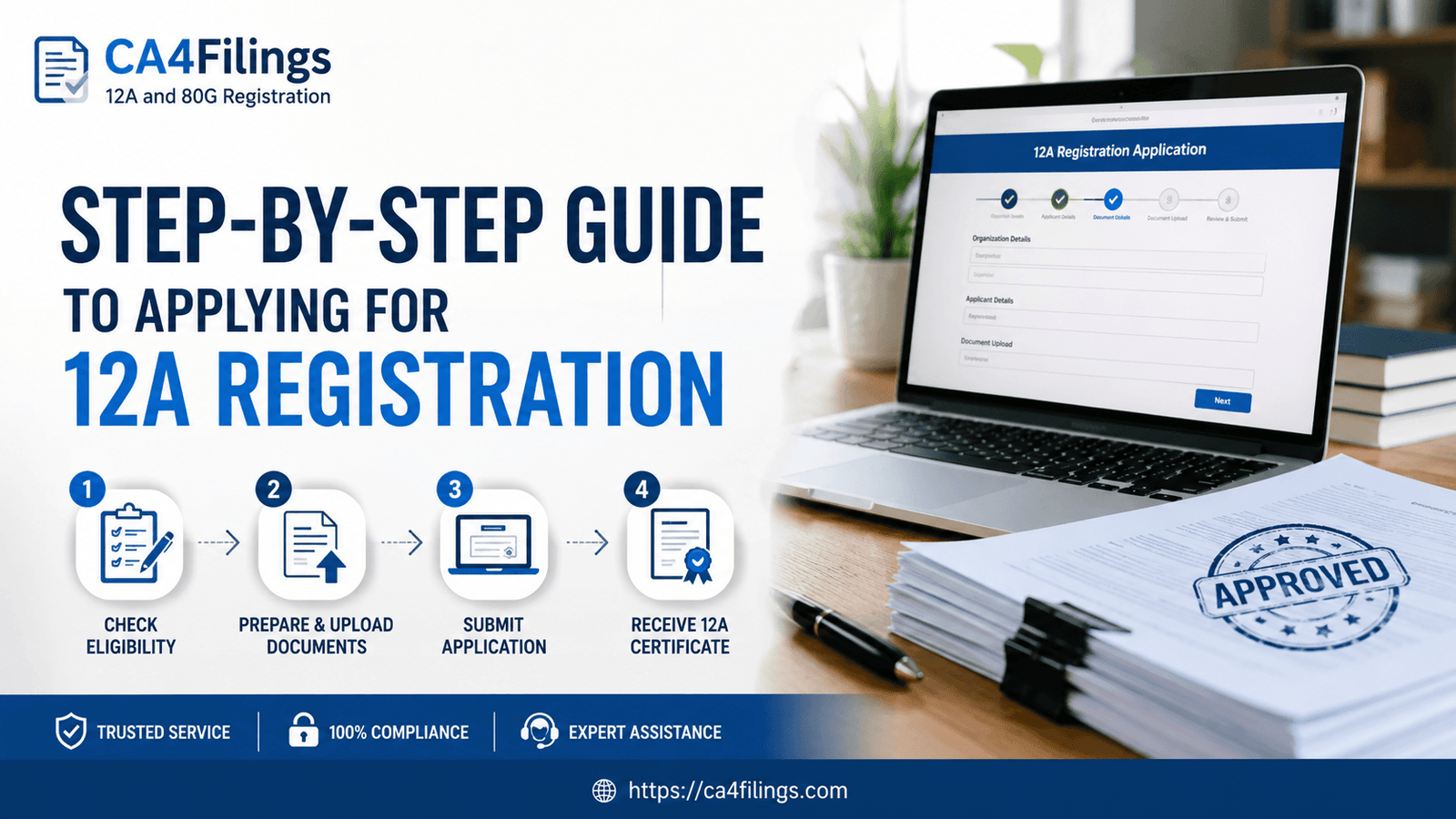

Step-by-Step Guide to Applying for 12A Registration

Once your documents are in order, it is time to initiate the actual application. Follow this practical, phase-wise breakdown to submit your application correctly.

Phase 1: Accessing the Portal

Go to the official Income Tax e-filing portal and log in using your organization’s unique PAN-based User ID and password. Ensure that the profile section is updated with the correct contact details of the primary authorized signatory.

Phase 2: Selecting the Correct Application Form

Navigate through the menu path: e-File > Income Tax Forms > File Income Tax Forms. Look for the section designated for charitable institutions. Now, you must choose your form based on your current operational status:

Select Form 10A if you are a brand-new entity seeking a fresh, provisional registration before commencing activities.

Select Form 10AB if you already hold a provisional registration and are applying to convert it into a regular, 5-year registration, or if you are renewing an existing regular registration that is nearing expiry.

Phase 3: Filling in the Core Details

The digital form requires meticulous data entry. You will need to carefully input the basic details of the organization, details of all current trustees/partners/directors, and the explicit legal sections under which registration is sought. You must also disclose structural asset-liability statistics and information regarding any other government portal registrations, like the NITI Aayog DARPAN portal.

Phase 4: Document Upload & Digital Verification

Upload all your self-certified attachments in the prescribed PDF layout. Once the fields show a completed green tick, proceed to verification. The form must be digitally signed by the authorized signatory using a Digital Signature Certificate (DSC) or verified via an Electronic Verification Code (EVC) linked to Aadhaar.

Once submitted, the system will generate an acknowledgment form containing a unique Document Identification Number (DIN). The Principal Commissioner or Commissioner of Income Tax (PCIT/CIT) will then evaluate your request. For a provisional application, the order is typically passed within one month from the end of the application month. For a final regular application, the official timeline allows up to six months from the end of the quarter in which you applied, during which the department might issue online clarifications or ask for supplementary activity logs.

Post-Registration Compliance Guidelines

Securing your certificate is an incredible milestone, but it is only half the battle won. To preserve your hard-earned tax-exempt status over the years, your organization must strictly follow essential Compliance Guidelines:

The 85% Application Rule: In any given financial year, your organization must utilize at least 85% of its total income directly toward its stated charitable or religious goals. If you fall short, the remaining unspent amount may become taxable unless it is legally accumulated or set aside for specific future projects using prescribed statutory forms.

Timely Tax Filings: Holding a 12A certificate does not mean you stop interacting with the tax department. You must file your annual Income Tax Return via ITR-7 every year before the specified legal deadline (usually October 31st).

Compulsory Audits: If the total income of your trust or institution exceeds the basic exemption limit (before claiming the benefits of Sections 11 and 12), getting your accounts audited by a practicing Chartered Accountant is legally mandatory. The audit report must be submitted online in Form 10B or Form 10BB.

Frequently Asked Questions

Q1. What is the official government registration fee for a 12A application?

There is no separate government Registration Fee or processing tariff levied directly on the Income Tax portal for filing Form 10A or Form 10AB. However, organizations usually budget for professional service fees when outsourcing the legal documentation, deed modifications, and filing work to specialized advisory firms like CA4Filings to prevent errors.

Q2. Can a private or family trust apply for this tax exemption?

No. Private or family trusts created for the financial benefit of specific relatives or private individuals are strictly ineligible for 12A benefits. The trust must be a public trust that openly serves the community at large without discrimination.

Q3. What happens if we miss the deadline to convert our provisional registration?

If your entity holds a provisional registration, you must apply for regular registration through Form 10AB either within six months of commencing your charitable activities or at least six months before the 3-year provisional period expires—whichever occurs earlier. Missing this timeline can lead to your provisional status lapsing, making your global income completely taxable at maximum rates.

Q4. Is a 12A certificate valid forever?

No, the perpetual validity model has been replaced. Fresh provisional certificates are valid for 3 tax years, while regular, final certificates are valid for 5 tax years. You must proactively file for renewal at least six months prior to the date of expiry.

Securing Your Organization's Financial Future

Navigating the nuances of tax laws can feel overwhelming when your primary passion lies in creating social change on the ground. However, executing this Step-by-Step Guide to Applying for 12A Registration seamlessly is the only definitive way to build a financially secure, highly credible, and compliant institution.

From analyzing your trust deed’s irrevocability clauses to filling out detailed application codes on the tax portal, precision is paramount. A single mismatched document or incorrectly selected section code can lead to tedious department queries or outright rejection. Let our expert team handle your regulatory stress. Connect with CA4Filings today, and let us manage your end-to-end tax compliance while you focus entirely on driving your social mission forward!

Latest Updates

ca4filings.com Services

-registration.png)